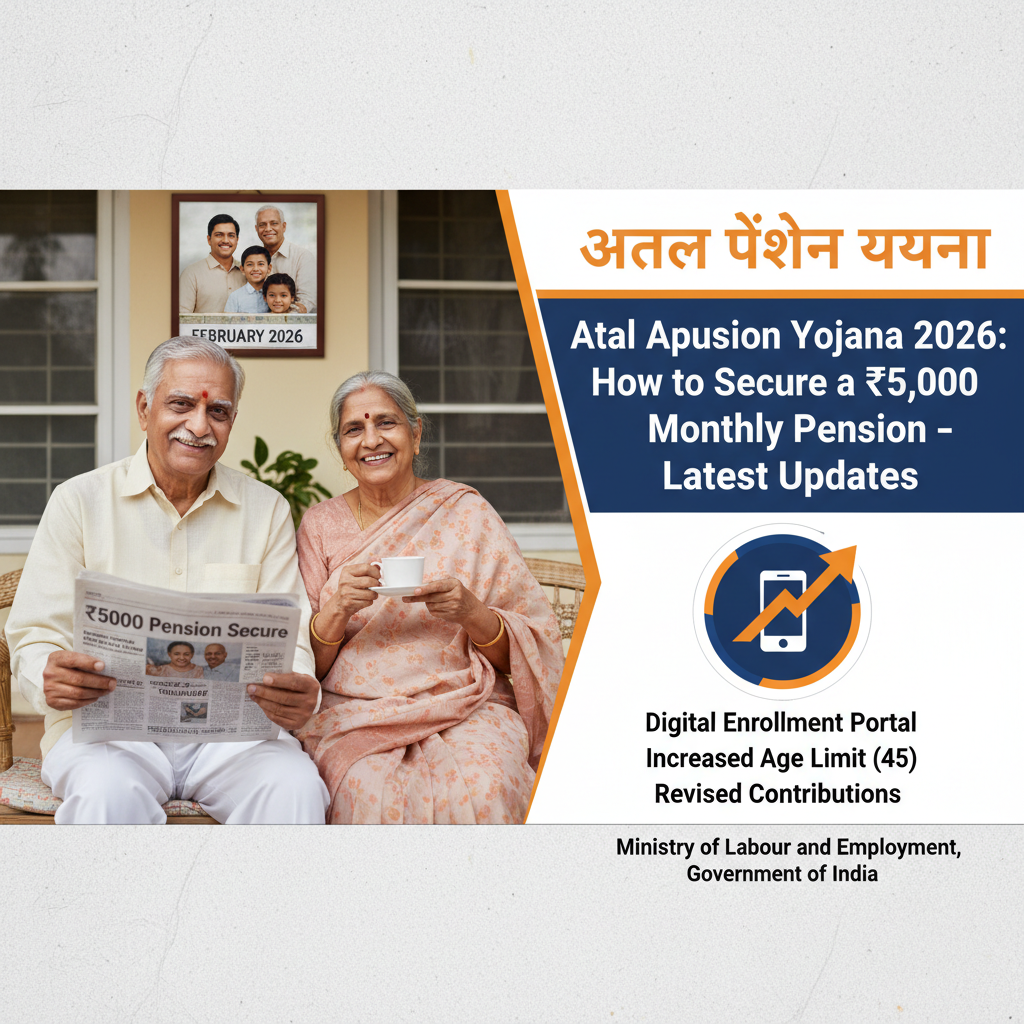

What is Atal Pension Yojana?

The Atal Pension Yojana (APY) is a government‑backed social security initiative launched in 2015 to provide a guaranteed monthly pension to senior citizens aged 60 and above. Funded by the Ministry of Labour and Employment, the scheme targets workers in the informal sector who lack access to any statutory pension. By allowing voluntary, flexible contributions, APY aims to create a reliable income stream for retirees, especially in rural and semi‑urban areas where traditional pensions are scarce. The program is closely aligned with other national financial inclusion missions such as the Pradhan Mantri Jan Dhan Yojana, reinforcing the vision of a comprehensive safety net for all citizens.

Who Can Join? Eligibility and Contribution Mechanics

Eligibility for APY is straightforward: the applicant must be an Indian resident, possess a valid bank account linked to an Aadhaar number, and be between 18 and 45 years of age at the time of enrollment (the upper limit was raised from 40 to 45 in 2026). The scheme is open to all workers, including daily‑wage labourers, street vendors, and small‑scale entrepreneurs, who do not already receive a statutory pension.

Contributions are flexible and can be made monthly, quarterly, or semi‑annually. The amount payable depends on two variables – the subscriber’s age at entry and the pension amount they wish to receive, which can range from a minimum of ₹1,000 to a maximum of ₹5,000 per month. For illustration, a 25‑year‑old who opts for the maximum ₹5,000 pension will need to contribute roughly ₹2,000 per month for about 35 years to accumulate the required corpus. This contribution schedule ensures that the accumulated fund can reliably deliver the promised pension without default risk.

Upon enrollment, the subscriber receives a unique identifier and an acknowledgment receipt. In the event of the subscriber’s death, the spouse becomes eligible to receive the same pension for life, provided they meet the eligibility criteria. Additionally, a nominee may receive a lump‑sum payout equal to the total contributions made, plus accrued interest, under specific circumstances.

2026 Updates: Higher Age Limit, Revised Rates and Online Portal

In February 2026, the Ministry of Labour and Employment announced three pivotal enhancements to APY. First, the upper age ceiling for new subscriptions was expanded from 40 to 45 years, enabling middle‑aged workers to plan for retirement later in life. Second, contribution rates were recalibrated to keep pace with inflation and market dynamics, safeguarding the long‑term solvency of the pension fund. Third, a fully digital enrollment platform was introduced, accessible via the official APY website and the UMANG mobile application, allowing applicants to complete the entire registration process online without visiting a branch office.

The online portal streamlines the procedure: users log in with an Aadhaar‑linked mobile number, select their desired pension amount, input personal details, and link their bank account. The system automatically calculates the required contribution based on the chosen pension and age, then generates an acknowledgment receipt and a subscriber ID. This digital shift has dramatically reduced enrollment time, cutting the average registration duration from several days to under an hour.

For more detailed information on the scheme’s official updates, visit the government’s labour portal at labour.gov.in.

Real‑World Impact: Pension Coverage and Citizen Benefits

Since its inception, APY has witnessed robust growth, with over 10 million beneficiaries receiving monthly pensions as of early 2026 – a 25 percent increase compared to the previous year. This surge reflects both higher enrollment rates and the effectiveness of recent policy interventions. The scheme has been particularly transformative for senior citizens in rural regions, where traditional pension coverage is often negligible. Recipients report improved financial stability, enabling them to meet basic needs such as healthcare, nutrition, and housing without relying on family support.

Beyond individual security, APY contributes to broader economic resilience. By guaranteeing a steady income for retirees, the scheme reduces poverty among the elderly and alleviates pressure on informal caregiving networks. Moreover, the predictable pension payouts stimulate local economies, as beneficiaries tend to spend their monthly allowances on goods and services within their communities.

Experts highlight the scheme’s role in bridging the gap between informal sector earnings and formal pension coverage. Dr. Anjali Mehta, a senior fellow at the Indian Institute of Public Administration, notes that “APY’s success hinges on sustained government commitment, robust financial management, and continuous outreach to unbanked populations.”

Challenges, Outlook and How to Enroll Today

Despite its achievements, APY faces several challenges that require strategic attention. Long‑term funding sustainability is paramount, especially as the population ages and the number of beneficiaries expands. Ensuring adequate contributions from younger workers while maintaining the promised pension levels demands vigilant fiscal oversight. Additionally, awareness campaigns are essential to reach out‑of‑school and unbanked segments, particularly in remote villages where digital literacy remains low.

To enroll, prospective subscribers can follow a simple three‑step process: visit the official APY website or download the UMANG app, complete the Aadhaar‑linked registration, select the desired pension amount, and link a bank account. After the first contribution is debited, the system issues a subscriber ID and an electronic receipt. Ongoing contributions can be auto‑debited from the linked account, ensuring hassle‑free compliance.

Looking ahead, the government plans to integrate APY with other social security programmes, creating a seamless ecosystem that provides end‑to‑end financial protection for all citizens. Stakeholders are encouraged to stay informed about scheme updates and to spread awareness in their communities. By doing so, more Indians can secure a dignified retirement and contribute to a financially inclusive nation.

Stay updated with the latest Yojana schemes and government initiatives for better awareness and eligibility. For personalized guidance on accessing these benefits, reach out to us.