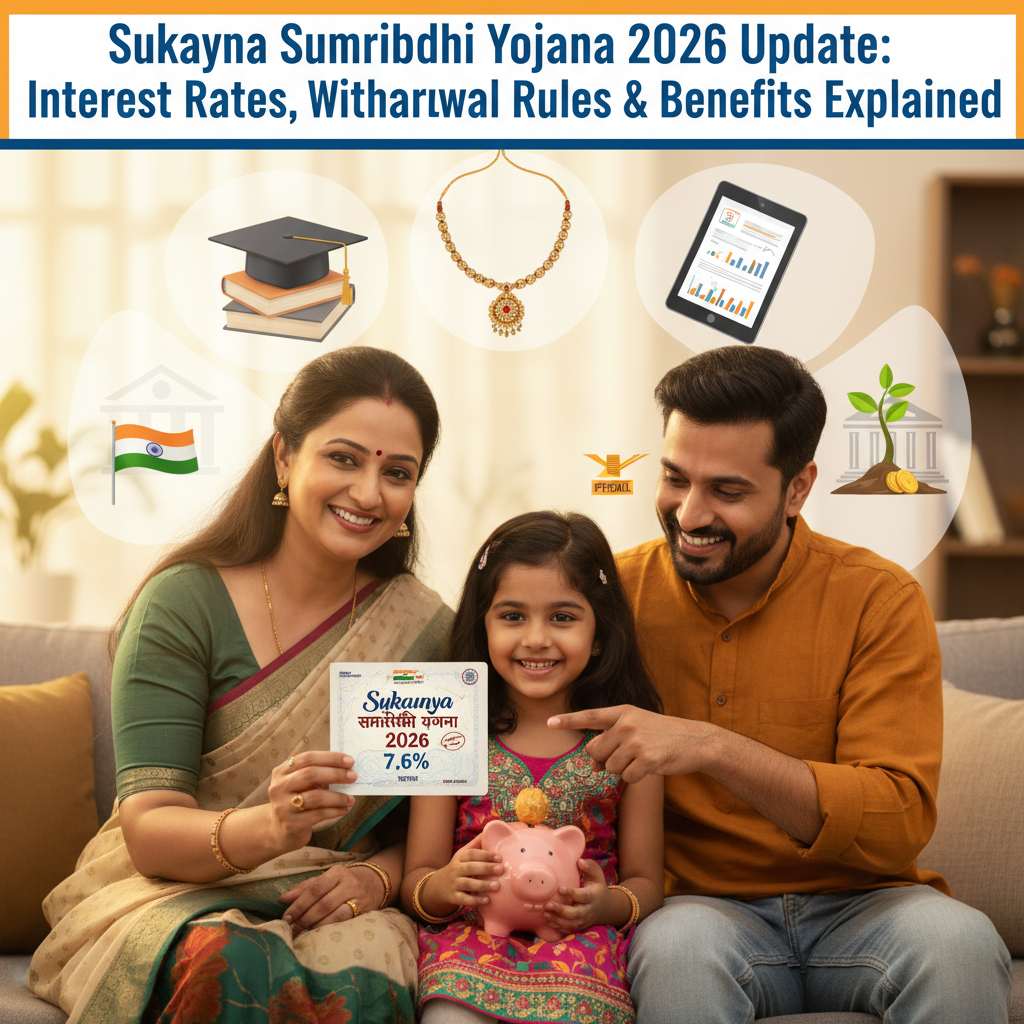

Overview of Sukanya Samriddhi Yojana 2026

The Sukanya Samriddhi Yojana (SSY) remains one of India’s most celebrated small‑savings schemes, designed specifically to secure the financial future of girl children. Launched in 2015 by the Ministry of Women and Child Development, the programme encourages families to build a dedicated corpus for education and marriage, offering a tax‑free interest rate, flexible deposit options, and a host of withdrawal benefits. In the 2026 fiscal year, the government announced an updated Sukanya Samriddhi Yojana interest rate 2026 of 7.6 % per annum,compounded annually, marking a modest rise from the 7.4 % rate prevailing in the previous year. This adjustment reflects the Reserve Bank of India’s effort to align small‑savings rates with market conditions while preserving the scheme’s long‑term sustainability. As a result, the SSY continues to be a cornerstone of financial planning for millions of Indian households.

Latest Interest Rate and Its Impact

Effective from 1 April 2026, the SSY interest rate stands at 7.6 % per annum, a figure that directly influences the growth of any deposited amount over the scheme’s 21‑year horizon. For illustration, a cumulative deposit of ₹1 lakh made at the time of account opening will grow to approximately ₹4.2 lakh after 21 years at the new rate, compared with roughly ₹3.9 lakh under the 7.4 % rate. This seemingly small 0.2 % increment translates into an additional ₹30,000‑₹35,000 in the final corpus, a significant margin when accounting for rising tuition fees and marriage expenses. Moreover, the interest earned is entirely tax‑exempt under Section 10(11) of the Income Tax Act, and contributions qualify for a deduction of up to ₹1.5 lakh under Section 80C, thereby enhancing the scheme’s attractiveness for middle‑class families seeking both savings and tax efficiency. The updated Sukanya Samriddhi Yojana interest rate 2026 thus not only safeguards the purchasing power of the accumulated funds but also equips families with a larger, inflation‑adjusted safety net for critical life events.

Withdrawal Rules and Conditions

One of the most frequently asked questions about the SSY concerns its withdrawal flexibility. Partial withdrawals become permissible once the girl child attains the age of 18 years, subject to a ceiling of 50 % of the account balance at that juncture. These funds can be mobilised for higher education or marriage-related expenses, provided the account holder submits supporting documentation such as a fee structure, admission letter, or marriage invitation. Full withdrawal is allowed after the girl turns 21 years, or upon her marriage, whichever occurs earlier, and the entire accrued balance—including interest—becomes payable. Premature closure before the stipulated age incurs a penalty: the interest rate for the remaining period is reduced by 1 %, and the account must remain active for a minimum of five years to avoid any deductions. These provisions ensure that the scheme remains a long‑term instrument while still offering practical liquidity when families need it most.

How to Open and Manage an SSY Account

Opening an SSY account is a straightforward process that can be undertaken at any post office or authorised bank branch across the country. An adult—typically a parent or legal guardian—can open an account in the name of a girl child who is not older than 10 years at the time of opening. The applicant must present identity proof, address verification, and a duly filled application form, accompanied by an initial deposit of at least ₹1,000. Subsequent contributions can be made in multiples of ₹100, up to a ceiling of ₹1.5 lakh per financial year, and may be deposited in cash, via cheque, or through electronic fund transfer. The interest is calculated quarterly and credited to the account, and the scheme permits nominations, allowing a legal heir to claim the benefits in the event of any untoward circumstance. Additionally, the account is portable; families relocating to a different state can transfer the SSY balance to another post office or bank without incurring any charges, ensuring uninterrupted growth of the corpus.

Key Benefits for Families and Future Outlook

Beyond the competitive Sukanya Samriddhi Yojana interest rate 2026, the scheme offers a suite of ancillary advantages that resonate with Indian families. The interest earned is completely exempt from taxation, and the deposit amount qualifies for a deduction under Section 80C, enabling substantial tax savings. The SSY also provides a low‑interest loan facility after the girl reaches 21 years, allowing borrowers to secure funds against the accrued balance at favourable rates. Moreover, the Ministry of Finance has signalled its intent to review the scheme’s rates annually, with discussions underway to raise the annual deposit ceiling to ₹2 lakh to keep pace with inflationary pressures on education and marriage costs. Integration with the Digital India initiative is also being explored, which could enable seamless online monitoring of balances, automated interest credits, and mobile‑based account management, thereby broadening financial inclusion and simplifying the experience for tech‑savvy parents.

Looking ahead, the government plans to enhance awareness through targeted campaigns and to streamline the claim process for withdrawals, ensuring that families can access funds for education or marriage with minimal bureaucratic delay. By aligning the scheme’s parameters with contemporary economic realities, the SSY aims to cement its position as a premier instrument for empowering the girl child and fostering gender‑balanced development across the nation.

Frequently Asked Questions

- Can I open an SSY account for a girl who is already 12 years old? The scheme permits account opening only for girls up to 10 years of age; however, existing accounts can continue to earn interest.

- Is there a limit on the number of deposits per year? No numerical limit exists, but the total annual contribution cannot exceed ₹1.5 lakh.

- What happens if I miss a deposit in a given year? The account remains active, but the missed deposit cannot be retrospectively added; the balance simply continues to earn interest.

- Can the account be transferred between post offices? Yes, transfers are allowed free of charge, and the process can be initiated online or at the respective branches.

- Does the scheme offer any loan facility? After the girl turns 21 years, a loan can be availed against the SSY balance at a low interest rate, providing additional financial flexibility.

Learn more about Sukanya Samriddhi Yojana on Wikipedia | Reserve Bank of India | Ministry of Finance

Stay updated with the latest Yojana schemes and government initiatives for better awareness and eligibility. For personalized guidance on accessing these benefits, reach out to us.