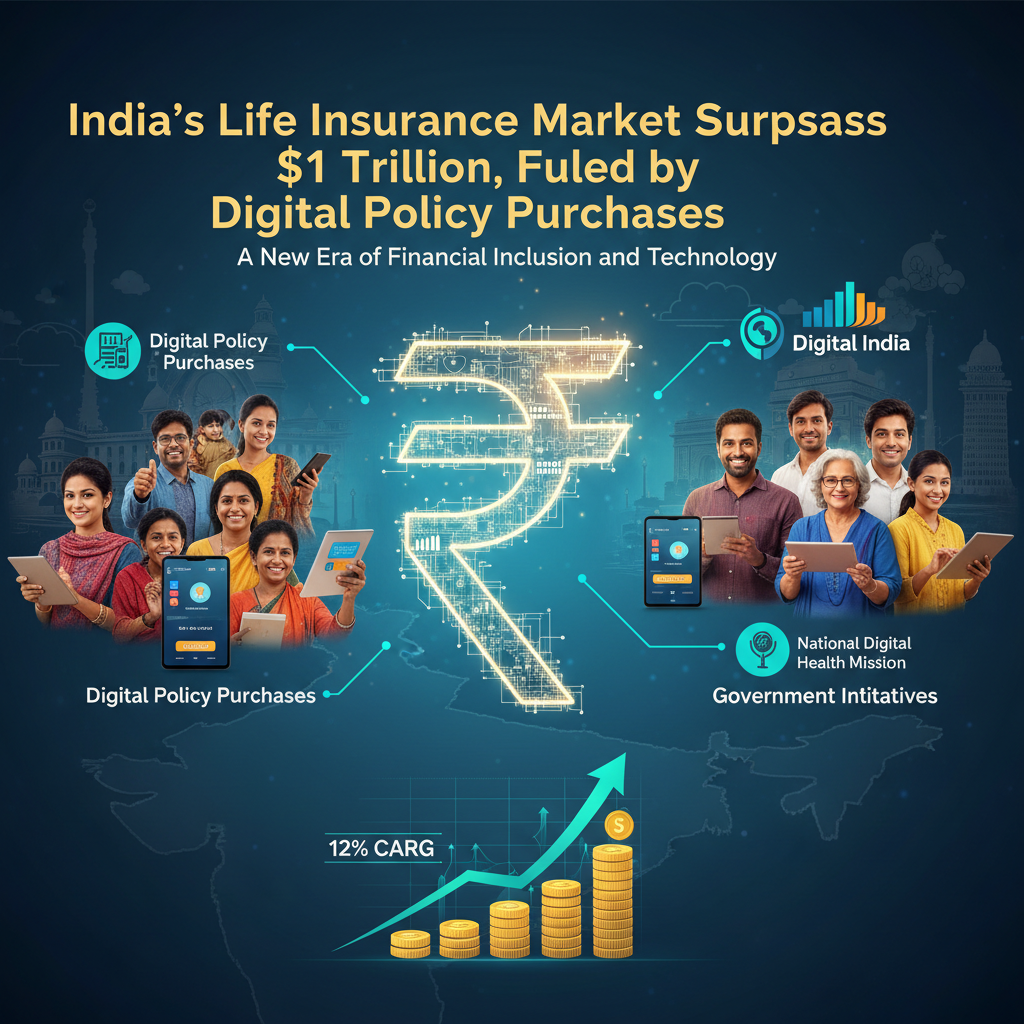

Market Milestone: $1 Trillion Valuation

India’s life insurance industry has crossed a historic $1 trillion threshold in terms of the total sum insured, marking a watershed moment for the country’s financial services landscape. According to the Insurance Regulatory and Development Authority of India (IRDAI) 2023 annual report, the aggregate coverage offered by life insurers now exceeds this figure, reflecting a compound annual growth rate (CAGR) of over 12 percent in the past five years. This surge is driven not only by rising income levels and urbanisation but also by a shifting perception of risk among households that increasingly view insurance as a cornerstone of long‑term wealth planning. The milestone underscores the sector’s transition from a niche product for the affluent to a mass‑market staple, positioning India alongside the world’s largest insurance markets such as the United States and China. As coverage expands, insurers are leveraging data analytics to tailor products, while policymakers see the growth as a catalyst for deeper financial inclusion.

Drivers of Digital Adoption

The acceleration of digital policy purchases is the primary engine behind the sector’s expansion. Mobile‑first platforms now enable consumers to obtain instant quotes, compare riders, and complete underwriting within minutes, eliminating the lengthy paperwork that once deterred first‑time buyers. Embedded insurance solutions — where coverage is offered at the point of sale through e‑commerce sites, travel portals, or fintech apps — have turned insurance into a seamless add‑on rather than a standalone transaction. This integration has broadened access for tech‑savvy demographics, especially Millennials and Gen‑Z, who prefer on‑demand, transparent pricing algorithms. According to a recent KPMG India study, digital channels accounted for 38 percent of new life insurance policies in 2023, up from 22 percent in 2019. The streamlined customer journey not only boosts the volume of policies sold but also raises the average ticket size, contributing directly to the $1 trillion valuation milestone.

Government Initiatives Boosting Insurance Penetration

Government programmes have created a fertile ecosystem for insurance uptake, especially among low‑income and rural populations. The Pradhan Mantri Jan Dhan Yojana has opened over 450 million bank accounts, many of which now serve as entry points for micro‑insurance products. Complementary schemes such as the Pradhan Mantri Jeevan Jyoti Bima Yojana provide affordable life cover to participants, while the National Digital Health Mission encourages integration of health insurance with broader financial planning. Tax incentives under Section 80C and Section 80D of the Income Tax Act further lower the effective cost of premiums, making policies more attractive to middle‑class families. Collectively, these initiatives have expanded the insurance net, enabling carriers to offer tailored, low‑premium products that resonate with previously untapped segments.

Shifts in Consumer Behavior and Regulatory Landscape

Consumer attitudes have undergone a profound transformation, accelerated by the COVID‑19 pandemic and heightened awareness of health and financial vulnerabilities. Surveys conducted by the Insurance Information Bureau of India reveal that 68 percent of respondents now prioritise life and health coverage for themselves and dependents, up from 45 percent in 2018. Social media influencers and fintech thought leaders have amplified narratives around wealth preservation, prompting interest in savings‑linked policies such as Unit‑Linked Insurance Plans (ULIPs). Regulators have responded with forward‑looking frameworks that balance innovation and consumer protection. The IRDAI’s sandbox policy allows insurers to test AI‑driven underwriting models under strict transparency rules, while recent amendments to the Foreign Direct Investment (FDI) policy have eased ownership caps, inviting global players to introduce cutting‑edge technologies. This regulatory environment nurtures competition and ensures that market growth aligns with safeguards against mis‑selling.

At the same time, the industry faces challenges around data privacy and consumer education. As insurers increasingly collect granular behavioural data to personalise pricing, robust cybersecurity measures become essential to protect sensitive health and financial information. To address potential knowledge gaps, industry consortia are developing standards for ethical AI use and deploying explainability tools that demystify complex policy terms for the average holder.

Future Outlook, Challenges and Conclusion

Looking ahead, analysts project that the life insurance sector could add another $500 billion in premium volume over the next three years, driven by deeper digitisation, expanded micro‑insurance offerings, and continued government focus on financial inclusion. The convergence of technology, policy, and consumer demand creates a virtuous cycle: innovation unlocks new customer segments, which in turn generates richer data that fuels further product development. However, sustaining this momentum requires vigilant management of data privacy concerns and a commitment to ongoing consumer education. Stakeholders — from insurers and regulators to policymakers — must strike a delicate balance between aggressive growth and responsible stewardship, ensuring that the benefits of a robust insurance market translate into tangible protection and prosperity for all citizens.

Stay updated with the latest Yojana schemes and government initiatives for better awareness and eligibility. For personalized guidance on accessing these benefits, reach out to us.